In the world of public pension funding and governance, good news is hard to come by. Maine’s levels of unfunded pension liabilities are no exception.

However, according to a report recently released by State Budget Solutions, a project of the American Legislative Exchange Council, Maine suffers what can loosely be described as the least bad unfunded pension liabilities in New England. While there is more work to be done, previous reforms (backed by the Maine Heritage Policy Center) and fiscal responsibility have contributed to a scenario in which the state’s pension system is slightly more manageable than many of its neighbors’.

Unaccountable and Unaffordable 2016 is a continuation of State Budget Solutions’ series of reports tracking levels of unfunded public pension liabilities in each of the 50 states. The crux of the report is that, thanks to loose slack afforded by government accounting standards and gimmicks perpetrated to veil the severity of the pension liabilities problem most states, the true debt owed on pension obligations is much greater than often reported in states’ annual reports. Specifically, the report shines a light on discount rates.

Broadly speaking, state pension systems pay for liabilities (benefits owed to retirees) by two main methods: accruing assets and investing those assets for a return. The discount rate represents how much of the liabilities are offset by the anticipated growth of assets through investment. There is nothing wrong with assuming that a well-governed plan’s assets will provide a return. Problems arise, however, when assumed rates of return are not consistently met.

If a plan’s administrators are expecting a certain percentage return on investment and actually earn much less, the unfunded portion of the plan’s liabilities will grow disproportionately to the state’s ability to offset them, exacerbating issues with overall debt. Unfortunately for most state-administered pension plans, that happens now more often than not. This failure to meet expected returns leads pension boards to chase ever-riskier investments in order to make larger gains to compensate for the previous year’s insufficient returns, a cyclical nightmare for the state. Additionally, the need to replenish the fund with new assets leads to the state’s pension fund taking revenues from other areas of government, creating difficulties for state budgeters and crowding out core services.

The report explains why State Budget Solutions relies on a much lower discount rate to calculate unfunded pension liabilities than typically found in state annual reports:

Given that many plans’ assumed rates of return are too high and invite risk, State Budget Solutions uses a more prudent rate of return…This study uses a rate of return based on the equivalent of a hypothetical 15-year U.S. Treasury bond yield…This year’s number is averaged from March 2015 to March 2016. The resulting rate is 2.344 percent, which is considered a “risk-free” rate. As the Society of Actuaries’ Blue Ribbon Panel recommends, “the rate of return assumption should be based primarily on the current risk-free rate plus explicit risk premia or on other similar forward-looking techniques.”

Unaccountable and Unaffordable applies this methodology when weighing unfunded liabilities for defined benefit plans because defined benefit plans are binding and guaranteed by the state. As such, a guaranteed benefit should be offset by a guaranteed, or risk-free, return.

State Rankings, Per Capita Obligations

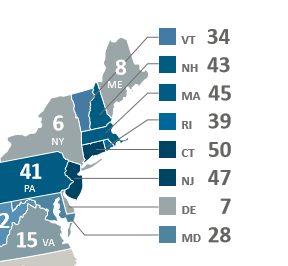

As stated above, Maine is comparatively better than the rest of New England for its funding ratio, which is the ratio of assets against liabilities. That said, the raw number is far from ideal. Maine ranks eighth in the nation, but with a mere 42.1% of its pension obligations funded. That said, no other New England state ranks above Vermont’s 30.4% ratio, which lands it at 34 out of 50. Connecticut ranks last, funding merely 22.8% of its liabilities.

While it is true that New Hampshire has the smallest per capita share of pension debt and Vermont has the smallest raw total of pension debt, Maine’s funding ratio is evidence of fiscal responsibility and a commitment to meeting its debts to prevent impacts on the state’s credit. That said, the generous benefits themselves are also drivers of unfunded liabilities, and in order to rescue pension systems on the whole, things like cost of living adjustments, overall rates of pensionable pay and retirement ages may need to be examined in Maine, as they should be everywhere.

Pursuant to a state constitutional amendment, Maine’s system must be fully-funded by 2028. While the need for reform is not extinguished and the system is far from fully rescued, requirements that are stronger than suggestions, or even mere statutes, are one of many paths to resolving the pension crisis ongoing all over the country.

The sooner pensions are rescued, the sooner states and municipalities can get back to the business of promoting growth and providing core services to their people.

Joe Horvath is a policy fellow at The Maine Heritage Policy Center. A resident of Connecticut, he serves as the assistant director of policy for the Yankee Institute for Public Policy. Previously, he worked as a research analyst for the American Legislative Exchange Council Center for State Fiscal Reform. His work has appeared in Bloomberg BNA, Tax Analysts and the Hartford Business Journal.