On October 7, 2024, the Committee for a Responsible Federal Budget (CRFB) presented a range of scenarios on how Vice President Harris and former President Donald Trump would affect the national deficit. The nation’s growing annual deficits and outstanding debt obligations have historically been a deeply important political issue. However, in recent years, interest in the issue has declined with both the general public and political candidates discussing the issue less and less. Before getting into the plans of each candidate, it is important to look at the history of this issue.

In the following figures below, years in red designate Republican control of both Congress and the White House, years in blue designate Democratic control of both Congress and the White House, and purple represents divided government (one party controlling either or both branches of Congress and a different party controlling the White House). Marked in a special dark red color is 2001 because the first half of the year featured a unified Republican government and the second half of the year featured a divided government.

Figure 1: Federal Deficit by Party Control Since 2000

The last time the United States ran a federal surplus was in 2001, when the federal government took in $130 billion more than it spent. Since then, annual deficits have progressively increased over time, rising with the outbreak of recessions and then decreasing when the economy stabilized. Concerningly, after the annual deficit peaked in 2020 during the pandemic, the United States is still running deficits well above pre-pandemic levels.

Clearly, both parties have been complicit in rising deficits. However, the longest period of deficit reduction (2011-2015) occurred under a Republican Congress and a Democratic president.

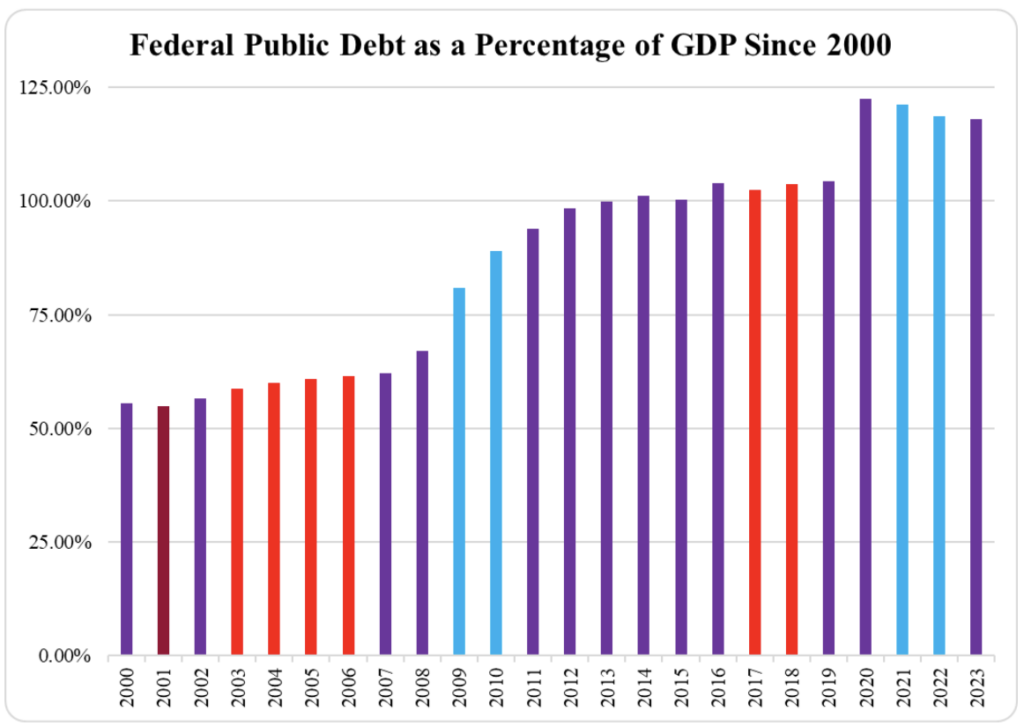

Figure 2: Federal Public Debt as a Percentage of GDP by Party

In addition to measuring a country’s annual deficits and surpluses, economists also look at the federal public debt as a percentage of GDP to assess a country’s fiscal health. Public debt is defined as all debt that the government owes to external parties. Total public debt, which is quite daunting at face value, is best taken in context with the size of the economy.

Still, many economists generally believe that debt exceeding 100% of GDP is problematic. In 2010, economists conducted a comparative study of countries across the globe and found that after public debt reaches 90% of GDP, economic growth slows substantially. Later on, after many countries passed this threshold, the architects of the study reiterated 90% was a rough estimate that could heavily vary by country. Some economists take a more optimistic tact, pointing to Japan’s over 200% debt to GDP ratio as a sign that public debt is of little concern. On the other hand, the University of Pennsylvania recently conducted a study stating that at its current pace, the United States cannot sustain current levels of spending for the next 20 years even if global conditions remain completely stable.

Other studies point to the opportunity costs present in borrowing, such as higher interest rates, lowering future growth, inflation, and the cost of servicing the debt. On the other hand, many economists argue that the United States can borrow comfortably at current rates due to its unique position in the global economy. The United States is far from the only country running large deficits, and it has the advantage of the U.S. dollar being the reserve currency in the world. Other economists will point out that the pain from national debt depends heavily on interest rates and that lower interest rates give the government more room to borrow. As of right now, interest payments on the debt represent the third largest line item in the federal budget.

Depending on one’s perspective, the current size of both the deficit and debt represent at best a tradeoff and at worst a path to a future fiscal crisis. At some point, it is possible the federal government will need to take some sort of action to lower deficits in order to stabilize public debt relative to GDP. Unfortunately, politicians, who are notorious for ignoring problems until either the last moment or after disaster has struck, have made little commitment on this issue. Complicating matters, there is no clear line designating how much debt is too much, only that the risk grows as public debt relative to GDP increases.

According to the CRFB, Vice President Harris’ tax and spending proposals under the most favorable scenario will keep the deficit on its current path, and at worst add an additional $8.10 trillion to outstanding debt during her potential presidency. Between these projections, the CRFB’s central projection predicts that a President Harris would add $3.50 trillion to the national debt in addition to current projections.

Former President Trump’s proposals are significantly worse on this issue. At the low end, President Trump’s proposals would add $1.45 trillion to the national debt beyond current projections. At the high end, $15.15 trillion would be added, with the central projection predicting a $7.50 trillion increase.

This discrepancy comes from President Trump’s desire to lower taxes without corresponding cuts in spending. Vice President Harris’ proposals, by contrast, increase spending but do not raise enough revenue to fully cover the cost, except for under the most optimistic estimates.

As the United States continues to borrow more and more money, the issue has been discussed less and less in our national politics. Ultimately, despite its lack of public discussion, the severity and urgency of the federal debt is fiercely debated by economists, although there appears to be a consensus that debt will have negative future consequences eventually – a fact that both parties seem content to ignore.

Connor Feeney, of South Portland, currently serves as a policy intern at Maine Policy. Connor is a fourth-year undergraduate student at the University of Southern Maine studying political science and economics, and is expected to graduate in December 2024.